For years, conventional personal finance advice in India has followed a predictable, repetitive script. Whenever inflation ticks upward, eroding the purchasing power of hard-earned savings, the immediate recommendation from generic market columnists is to blindly invest in diversified mutual funds via systematic investment plans.

While equity mutual funds remain an important vehicle for capital appreciation, treating them as a universal, one-size-fits-all shelter during inflationary cycles overlooks critical structural realities. Volatile market environments can severely test an investor’s emotional tolerance, and timing equity entry points requires patience.

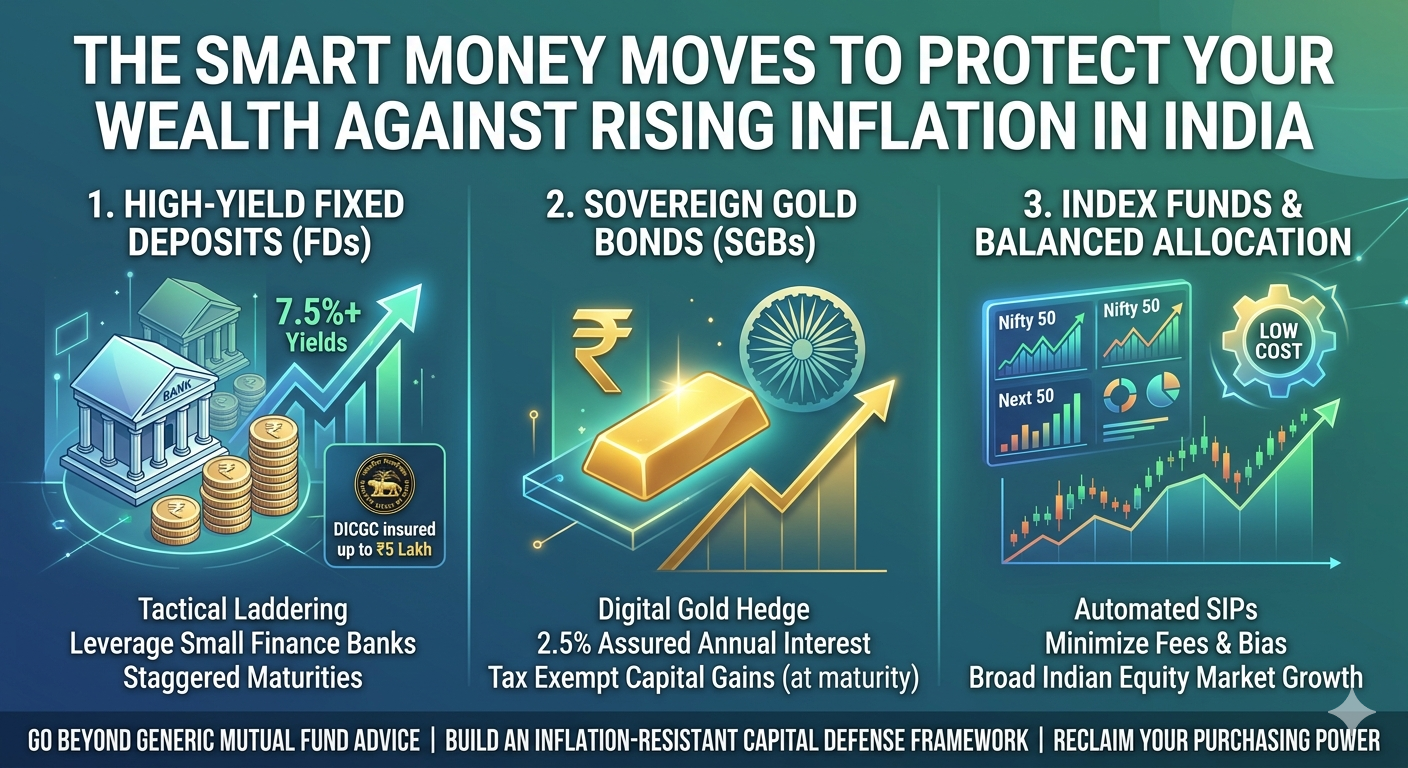

To achieve true capital preservation, savers must move past surface-level recommendations and adopt highly specific, modernized financial planning strategies. Safeguarding family wealth against rising consumer prices requires cutting through generic market commentary to implement a precise, three-pronged framework combining high-yield fixed income structuring, targeted digital sovereign assets, and automated, low-cost index allocation.

The High-Yield Fixed Deposit Strategy: Tactical Laddering

Many modern investors dismiss traditional fixed deposits as outdated, low-return vehicles that naturally lose value when adjusted for inflation. This critique is accurate if you simply leave massive lumps of capital languishing in standard savings accounts or long-term public sector bank deposits yielding under six and a half percent. However, fixed income remains the literal bedrock of capital safety, provided you deploy it tactically.

+--------------------------+------------------------+------------------------+

| Banking Segment | Average Yield Range | Strategic Utility |

+--------------------------+------------------------+------------------------+

| Major Public Sector Lenders| 6.10% to 6.60% | Maximum Baseline Safety|

| Established Private Banks| 6.50% to 7.35% | Balanced Yield Core |

| Small Finance Institutions| 7.40% to 8.11% | High Yield Accelerators|

+--------------------------+------------------------+------------------------+

The key to optimizing fixed income is utilizing small finance banks and select mid-sized private institutions, which are aggressively competing for domestic deposits by offering significantly higher yields. While top-tier public sector banks offer conservative rates, several scheduled small finance institutions provide highly competitive yields reaching up to eight percent or higher for specific short to medium-term tenures.

To maximize safety while chasing these yields, investors must leverage the Deposit Insurance and Credit Guarantee Corporation, a wholly-owned subsidiary of the Reserve Bank of India that guarantees principal and interest deposits up to five lakh rupees per depositor, per bank.

Instead of locking capital into a single ten-year deposit, smart financial planning dictates creating a structured fixed deposit ladder. Under this model, an investor breaks down their cash reserves into four separate tranches distributed across different institutions, with maturities staggered at six, twelve, eighteen, and twenty-four months. As each deposit matures, the capital is either deployed into emerging high-yield market opportunities or rolled over into the latest peak-rate tenure. This continuous cycle ensures consistent liquidity, mitigates interest rate risk, and creates a reliable cash flow engine that acts as a buffer against escalating consumer prices.

Capital Allocation in Sovereign Gold Bonds: The Digital Hedge

Gold has served as humanity’s definitive hedge against currency devaluation for thousands of years. However, storing physical gold bars or heavy jewelry inside domestic safes or commercial bank lockers introduces substantial security risks, immediate making charges, and steep liquidity discounts upon resale.

Sovereign Gold Bonds, issued directly by the Reserve Bank of India on behalf of the Central Government, completely eliminate these traditional structural frictions while amplifying overall asset returns. These government-backed digital securities are explicitly denominated in grams of gold, meaning your investment tracks the underlying spot price of the precious metal with absolute precision.

+-----------------------------------+-----------------------------------+

| Physical Gold Investment Frauds | Sovereign Gold Bond Architecture |

+-----------------------------------+-----------------------------------+

| Subject to heavy making charges | Zero manufacturing or storage fees|

| Purity verification risks at resale| Explicitly backed by sovereign state|

| Zero ongoing yield generation | Assured 2.5% fixed annual interest|

| Subject to capital gains taxation | Capital gains tax free at maturity|

+-----------------------------------+-----------------------------------+

The structural advantages of Sovereign Gold Bonds extend far beyond simple price tracking. While physical gold sits completely idle in a vault, these digital bonds pay an assured, fixed interest rate of two and a half percent per annum on the initial investment amount, credited semi-annually directly to the investor’s linked bank account.

Furthermore, the tax architecture is uniquely designed to reward long-term investors. For original subscribers who navigate the full eight-year maturity timeline, the entire capital gains tax arising from gold price appreciation is completely exempted. This unique combination of an underlying commodity hedge, sovereign backing, ongoing annual yield generation, and complete capital gains tax immunity makes digital gold an essential structural anchor for any inflation-resistant portfolio.

Balancing Index Funds: The Low-Cost Equity Engine

While fixed income and gold provide essential capital defense and safety, actively growing your purchasing power above the baseline rate of inflation requires a dedicated equity allocation engine. Instead of attempting to pick individual stocks or relying on expensive, actively managed mutual funds where high expense ratios quietly eat away at long-term compounding, modern portfolios should pivot decisively toward low-cost index funds.

Index investing operates on a transparent, rules-based philosophy. A standard Nifty Fifty or Nifty Next Fifty index fund simply replicates the exact composition of India’s largest corporate enterprises. This structural passivity keeps operational costs exceptionally low, with direct index fund tracking errors and expense ratios routinely sitting below zero point two percent, compared to the one to two percent fees demanded by active fund managers.

Over extended multi-year horizons, historical data consistently demonstrates that the vast majority of active fund managers fail to beat the benchmark index after accounting for their higher operational fees. By automating a monthly systematic investment plan into low-cost index funds, investors remove human bias, minimize structural costs, and tether a portion of their savings directly to the broader structural growth of the Indian economy.

Implementing the Three-Pronged Capital Defense Framework

True protection against inflation requires building a balanced financial ecosystem where assets complement each other across shifting economic cycles. A highly effective baseline capital allocation framework for a risk-aware investor involves distributing funds across fixed deposits, digital gold, and equities.

CAPITAL ALLOCATION MODEL

+------------------------+

| Total Liquid Capital |

+-----------+------------+

|

+-------------------+-------------------+

| | |

+--------v-------+ +--------v-------+ +--------v-------+

| Fixed Deposits | | Digital Gold | | Index Funds |

| (40% Core) | | (30% Hedge) | | (30% Growth) |

| Staggered SFB | | Sovereign SGBs | | Nifty 50 / SIP |

+----------------+ +----------------+ +----------------+

Under this balanced approach, forty percent of liquid capital is directed into high-yield fixed deposit ladders, establishing an insured, liquid cash core. Thirty percent is channeled into Sovereign Gold Bonds, creating a secure commodity buffer that performs exceptionally well during global geopolitical friction or currency volatility. The final thirty percent is channeled into automated index funds via systematic investment plans, providing the essential long-term growth engine required to beat core inflation.

This multi-layered approach ensures your money is never exposed to a single point of failure. If the stock market experiences a temporary cyclical downturn, your high-yield fixed deposits continue to generate predictable monthly cash returns. If consumer prices spike unexpectedly, your sovereign gold allocation appreciates in tandem to preserve your real-world purchasing power. Stop relying on simplistic, single-asset investment strategies; implement a diversified, modern financial blueprint to ensure your family’s financial security remains completely unassailable.