A viral social media post has shattered the illusion that a six-figure monthly income guarantees financial peace in urban India. A married couple in their early 30s took to Reddit with a raw, transparent breakdown of their finances, titled “Earning 1.7L, living paycheck to paycheck, mentally exhausted, need actionable input.”

The post quickly went viral across platforms, igniting a fierce debate on lifestyle choices, rising urban living costs, and the unseen financial burdens borne by young Indian professionals.

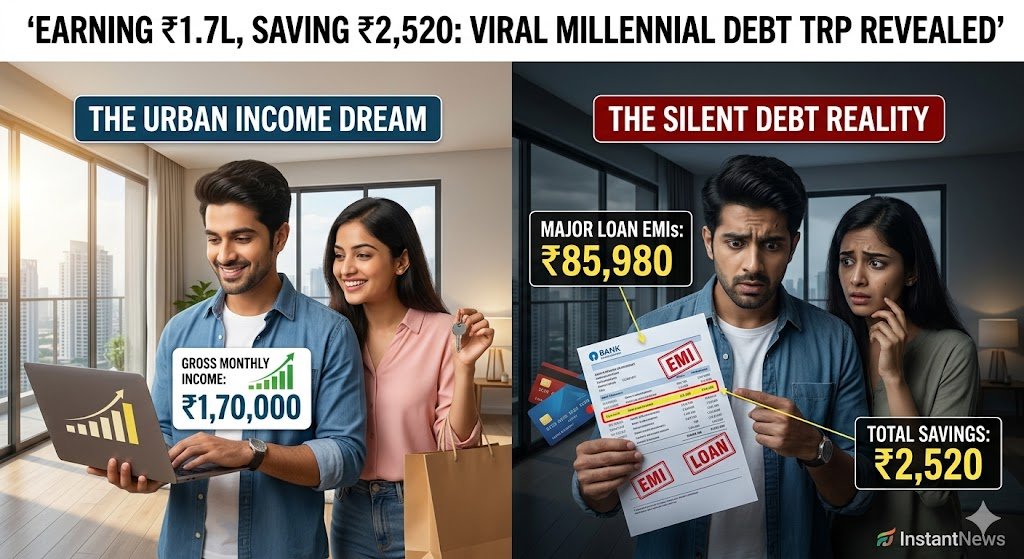

The Math: Where Does ₹1.7 Lakh Go?

On paper, the couple is comfortably in the upper-middle-class bracket. The husband brings home ₹1.02 lakh per month, while the wife earns ₹68,000, bringing their combined post-tax income to ₹1.7 lakh.

However, a closer look at their monthly ledger reveals a staggering leak: loans.

| Expense Category | Monthly Cost (₹) | Key Details |

| Total Debt EMIs | ₹85,980 | Includes a massive personal loan (₹70,154), education loan (₹3,000), bike loan (₹12,000), and a phone EMI (₹826). |

| Fixed Household Expenses | ₹53,500 | Covers rent, society maintenance, groceries, daily travel, utilities, and medical bills. |

| Variable Spending | ₹28,000 | Allocated for personal spending, occasional dining out, leisure, and family emergencies. |

| Net Monthly Savings | ₹2,520 | Remaining balance at the end of the month. |

The couple expressed deep anxiety about their future, asking questions that echo the fears of an entire generation: “Where do I even start fixing this? How do we plan for a house? When do we plan for kids? Our finances will be better after two years, but it feels like time is running out.”

The Twist: It’s Not Just “Lifestyle Creep”

While initial comments on the viral thread heavily criticized the couple for taking EMIs on luxury items like smartphones and a new electric bike, the husband later clarified a heartbreaking reality that many young Indians face: family debt inheritance.

The overwhelming bulk of their debt—the ₹70,154 monthly personal loan payment—stems from a ₹30 lakh loan the husband took out to consolidate his parents’ high-interest debts. Local lenders were charging his family interest rates as high as 18%, forcing him to step in and refinance the crisis with a personal loan at 13%.

What looked like irresponsible millennial spending on the surface was actually the financial toll of acting as a familial safety net.

The Internet Divides: Career Switch vs. Aggressive Snowballing

The financial reality check drew a flood of contrasting advice from the internet:

- The Aggressive Debt Paydown: Many users advised attacking the smaller liabilities immediately. Clearing the phone and bike EMIs over the next few months would free up ₹13,000 in monthly cash flow, which could then be aggressively channeled into prepaying the massive personal loan.

- The “Income is the Only Remedy” Stance: Tech professionals on the thread argued that the couple, given their ages and locations, are likely underpaid. One user noted, “There is only one way to fix your condition: Switch companies for a higher CTC. Increasing your primary income is the ultimate fix.”

The Bigger Picture for Urban India

This viral breakdown highlights a growing phenomenon among urban Indian millennials: the squeeze between high debt obligations, surging metropolitan living costs, and the cultural expectation to support aging parents. For many, a six-figure salary is no longer a ticket to luxury—it is simply the baseline required to keep their heads above water.

Frequently Asked Questions

Part 1: Decoding the Viral ₹1.7 Lakh Budget Breakdown

Q1. What is the viral ₹1.7 lakh income vs ₹2,520 savings story trending in India?

It originates from a viral financial breakdown shared by a 30-year-old married working couple in an urban Indian city. Despite a high combined monthly post-tax take-home pay of ₹1.7 Lakh, their massive debt obligations leave them with just ₹2,520 at the end of the month, sparking a massive national debate on middle-class survival.

Q2. How much do the individual partners earn in this viral trending couple?

The husband earns a monthly net salary of ₹1.02 Lakh, and the wife earns a monthly net salary of ₹68,000, bringing their combined monthly disposable income to exactly ₹1,70,000.

Q3. Where does the majority of the couple’s ₹1.7 Lakh monthly income go?

The absolute bulk of their salary goes toward servicing various debt obligations. Their total monthly Equated Monthly Installments (EMIs) consume a staggering ₹85,980—accounting for just over 50.5% of their total income.

Q4. What are the specific loan breakdowns for the viral millennial couple?

Their monthly loan repayment schedule consists of:

- A major personal loan EMI: ₹70,154

- A two-wheeler/bike EMI: ₹12,000

- An education loan EMI: ₹3,000

- A smartphone EMI: ₹826

Q5. Why did the husband take out a massive ₹30 lakh personal loan?

The husband took out the ₹30 Lakh personal loan at a 13% interest rate to consolidate and pay off his parents’ chaotic debts. Local, informal predatory lenders were charging his family up to 18% interest, creating an immediate family emergency.

Q6. Is the viral couple’s hand-to-mouth situation caused purely by “lifestyle creep”?

No. While they face minor lifestyle inflation via electronic and vehicle EMIs, the root cause is structural familial debt inheritance. Over 41% of their entire monthly income goes purely to paying off the loan taken for the husband’s parents.

Q7. How much does the trending couple spend on mandatory household expenses?

Their fixed monthly household bills total ₹53,500. This includes rent, society maintenance, basic groceries, daily commuting expenses, utilities (electricity, internet), and ongoing family medical bills.

Q8. What is the couple’s monthly variable “fun” budget?

They allocate ₹28,000 per month for personal expenses, dining out, ordering food, weekend leisure, clothing, and an ad-hoc pool for unexpected family emergencies.

Q9. What city does this couple live in, based on their expenses?

While the exact location was kept confidential for privacy, financial experts tracking the thread note that a rent-and-maintenance baseline of ₹25,000 to ₹30,000 points directly to a Tier-1 Indian metro city like Bengaluru, Mumbai, Pune, or Delhi-NCR.

Q10. What specific anxieties did the couple express in their viral post?

The couple highlighted deep mental exhaustion, stating they feel trapped. They expressed panic over how they will ever manage milestones like saving for a home downpayment, funding future children, or managing emergency medical scares with only ₹2,520 saved per month.

Part 2: The Hidden Indian Debt Trap & Family Realities

Q11. What is “familial debt inheritance” in the context of Indian millennials?

It is a common cultural dynamic where young urban professionals take on legal and financial liability (via bank personal loans or credit cards) to bail out their aging parents from informal debts, business losses, or medical crises.

Q12. Why do young Indian professionals resort to bank personal loans to clear parental debt?

Informal lenders in Indian towns and cities often charge unregulated, compounding interest rates between 18% and 36%. Refinancing that debt through a structured banking personal loan at 12% to 14% stops the predatory cycle, even if it severely damages the child’s cash flow.

Q13. How common is the “Sandwich Generation” crisis among urban Indians?

It is exceptionally common. Indian millennials act as a “sandwich” layer—they must simultaneously financially support their aging parents (who often lack robust pensions or health insurance) while trying to fund their own children’s future and skyrocketing urban living costs.

Q14. What is the average interest rate on a personal loan in India?

Depending on an individual’s credit score (CIBIL) and employment status, personal loan interest rates typically range from 10.5% to as high as 24% per annum.

Q15. Why are informal, local lenders in India so dangerous for middle-class families?

Local money lenders operate outside institutional banking frameworks. They rely on high-interest structures, daily or weekly compounding systems, and aggressive personal recovery tactics that can decimate a family’s mental peace and financial security.

Q16. Can a bank deny a personal loan if it is for parent debt clearance?

Banks look primarily at your CIBIL score, debt-to-income ratio, and repayment capacity. They do not usually restrict the loan based on personal usage, which is why individuals use them for family debt consolidation.

Q17. How does a massive personal loan impact an individual’s credit profile?

A high-value personal loan increases an individual’s credit utilization and total debt burden. If your monthly EMIs cross 50% of your net income, banks categorize you as “high risk,” making future home or car loans incredibly difficult to secure.

Q18. How can a family avoid falling into high-interest informal debt loops?

The primary defenses are setting up a dedicated emergency medical fund, purchasing comprehensive standalone parental health insurance early in life, and avoiding informal chit funds or unverified local business investments.

Q19. What is debt consolidation, and when should an individual use it?

Debt consolidation is the process of taking out a single, lower-interest loan to pay off multiple smaller, high-interest debts. It simplifies monthly tracking into a single EMI and reduces the overall interest paid over time.

Q20. Is it legally mandatory for Indian children to pay off their parents’ personal debts?

No. Legally, unsecured debts of a parent do not automatically pass to the children unless the child signed as a co-borrower or guarantor. However, deep cultural obligations and social pressure drive most Indian children to willingly step in.

Part 3: Urban Cost of Living & The “Millennial Lifestyle Creep”

Q21. What is “lifestyle creep” (lifestyle inflation)?

Lifestyle creep occurs when an individual’s discretionary spending increases in lockstep with their rising income. Things that were once viewed as luxury items (like premium gym memberships, daily barista coffee, or hailing cabs over taking metro rides) gradually turn into non-negotiable monthly “needs.”

Q22. Is a monthly salary of ₹1.7 lakh considered rich in urban India?

Statistically, a household income of ₹1.7 Lakh per month places a family in the top 5% to 10% of India’s income distribution. However, in Tier-1 cities, high rental costs, tax brackets, and essential services reduce its actual purchasing power significantly.

Q23. What are the average fixed living expenses for a couple in a Tier-1 Indian city?

For a comfortable middle-class life, typical monthly expenses run between:

- Rent/Maintenance: ₹22,000 – ₹40,000

- Groceries & Household Supplies: ₹8,000 – ₹12,000

- Utilities & Wi-Fi: ₹3,000 – ₹5,000

- Commuting/Fuel: ₹4,000 – ₹7,000

Q24. Why are zero-savings habits becoming a trend among high-earning corporate workers?

The rise of “Instant Gratification” culture, paired with frictionless digital payment ecosystems (UPI, “Buy Now, Pay Later” apps, and instant credit card approvals), makes impulsive discretionary spending effortless, leading to the ” paycheck-to-paycheck” loop.

Q25. How much does a couple typically need to live comfortably in Delhi, Mumbai, or Bengaluru?

Without debt burdens, a monthly net income of ₹70,000 to ₹90,000 allows a married couple to cover rent, utilities, insurance, and dining out while preserving a healthy margin for investments.

Q26. Why do electronic and gadget EMIs trap people into living paycheck to paycheck?

No-cost EMIs look appealing because they slice a ₹80,000 smartphone into a “small” payment of ₹6,600 over 12 months. However, stacking 3 or 4 of these micro-EMIs simultaneously subtly eats away at a professional’s foundational monthly savings margin.

Q27. Does renting an apartment make more financial sense than paying a home loan EMI in India?

In most Tier-1 Indian cities, the rental yield is very low (around 2% to 3%), whereas home loan interest rates hover around 8.5% to 9.5%. Renting is often dramatically cheaper on a month-to-month cash flow basis than committing to a 20-year home loan EMI.

Q28. How does inflation impact the monthly grocery and utility budget of urban households?

With retail inflation trends impacting essential food items and electricity tariffs across states, urban households have seen their baseline grocery and utility costs swell by roughly 15% to 20% over the last few years.

Q29. What is the financial risk of relying completely on corporate health insurance?

If you lose your job or decide to pivot careers to build a business, you instantly lose your medical cover. Furthermore, corporate health policies rarely provide adequate coverage for specialized, long-term treatments for aging parents.

Q30. Why do variable expenses like dining out or ordering food online go unnoticed in budgets?

Because micro-transactions made through UPI apps for food delivery apps, quick-commerce groceries, and quick weekend meetups feel small individually (₹300 here, ₹500 there), but aggregate silently into ₹20,000+ leaks at the end of the month.

Part 4: Expert Financial Solutions & Actionable Advice

Q31. What is the “Debt Snowball” method for paying off loans?

The Debt Snowball strategy involves listing all your debts from the smallest balance to the largest. You pay the absolute minimum on all large loans and throw every single extra rupee of available cash to wipe out the smallest loan first. This builds rapid psychological momentum.

Q32. What is the “Debt Avalanche” method, and how does it work?

The Debt Avalanche strategy prioritizes listing loans strictly by their interest rates. You aggressively pay off the loan carrying the highest interest rate first (such as a 24% credit card or 14% personal loan) to minimize the absolute total interest paid over time.

Q33. How can the viral couple free up cash flow immediately?

They should focus on eliminating their two smallest liabilities right away: the smartphone EMI (₹826) and the bike EMI (₹12,000). Clearing these two balances instantly injects nearly ₹13,000 of free cash flow back into their monthly bank account.

Q34. What is a “bare-bones” or “emergency” lockdown budget?

A temporary, aggressive lifestyle reduction where all non-essential, variable luxury spending (subscriptions, dining out, weekend leisure, gourmet foods) is paused completely. Every available rupee is channeled into liquid safety cash or rapid debt prepayment.

Q35. What percentage of a monthly salary should ideally go toward investments?

The gold standard for stable financial planning is the 50/30/20 rule: 50% of your income goes to essential needs, 30% to discretionary wants, and a minimum of 20% should be funneled straight into long-term investments and savings.

Q36. Should an individual prioritize investing or paying off high-interest debt?

If the debt carries an interest rate higher than 10% (like personal loans or credit cards), you should prioritize paying it off immediately. Very few safe, retail investment options can reliably beat a guaranteed 10%+ negative drag on your wealth.

Q37. How can a professional safely negotiate or restructure a personal loan with a bank?

If your cash flow is under severe distress, you can approach your lending bank to request a loan restructuring. This involves extending the loan tenure to drop the monthly EMI price, or asking for an interest rate conversion based on an improved CIBIL score.

Q38. What is the ideal size for an urban household’s emergency fund?

An emergency fund should hold liquid cash equivalent to 6 to 9 months of your total fixed living expenses plus mandatory loan EMIs, tucked safely away in a high-yield savings account or liquid mutual fund.

Q39. How can young couples balance supporting parents without destroying their own futures?

By establishing clear, boundaried financial conversations early on. Families should pool assets where possible, transition parents onto senior-citizen public health schemes, and ensure children do not take on structural debts that outpace their own primary salary growth.

Q40. Why do financial experts advise changing companies to fix a debt crisis?

When fixed loan EMIs are locked in, reducing your expenses can only save you a few thousand rupees. Conversely, switching jobs for a 30% to 50% hike in corporate India can instantly inject an extra ₹30,000 to ₹50,000 of fresh income directly into your monthly debt clearance engine.

Part 5: Reader Reflection & Community Conversation Starters

Q41. Why has this viral post split opinion across Indian internet spaces?

Because it challenges our assumptions about money. Half of the internet blames the couple for lack of financial discipline and buying lifestyle assets on credit, while the other half deeply empathizes with the harsh realities of corporate burnout and inescapable family obligations.

Q42. What does this trending debate reveal about corporate work culture and salary inflation?

It highlights that high corporate salaries in India often come hand-in-hand with immense mental exhaustion. When professionals work 60-hour weeks, they often use luxury spending as a therapeutic coping mechanism (“revenge spending”), which worsens the paycheck-to-paycheck cycle.

Q43. How can I track my own hidden monthly financial leaks?

The most reliable method is to review your bank and UPI statements at the end of the month. Categorize every transaction into “Needs,” “Wants,” and “Debts” to clearly see exactly where your hard-earned money is slipping away.

Q44. What is the psychological toll of living paycheck-to-paycheck on a high income?

It creates severe cognitive dissonance and chronic anxiety. Individuals feel deep shame because they know they earn a great income on paper, yet they live with the constant underlying terror of a single medical emergency or job layoff collapsing their entire life.

Q45. Are modern financial goals like early retirement (FIRE) realistic for the average Indian millennial?

Achieving Financial Independence, Retire Early (FIRE) remains realistic, but it demands an entirely debt-free lifestyle, high baseline discipline, and avoiding major lifestyle creep during your peak earning years between ages 25 and 35.

Q46. How can a couple talk about money transparently without fighting?

By setting up regular, low-stakes monthly financial check-ins. Frame the conversation around shared milestones (trips, safety nets) rather than tracking or policing individual spending slips.

Q47. What are the warning signs that you are entering a dangerous debt trap?

- You use one credit card to pay off another.

- You consistently pay only the “Minimum Amount Due” on credit card statements.

- Your total monthly EMIs cross 40% of your net monthly take-home pay.

Q48. How does peer pressure on apps like Instagram fuel lifestyle creep in India?

Seeing peers showcase luxury vacations, designer clothing, aesthetic cafe visits, and brand-new cars triggers a subconscious desire to match their consumption habits, frequently funded by hidden high-interest credit card debt.

Q49. What is the very first step to take if you realize you are broke despite a high salary?

Accept the reality without shame, download your last three months of bank statements, face the exact numbers, and freeze any option for new credit or EMIs immediately.

Q50. Where can readers share their own thoughts and local expense sheets on this topic?

Join the trending discussion in our comment section below! Share your monthly metro living expenses, your strategies for handling family responsibilities, and let us know: Could you survive comfortably on a ₹1.7 Lakh salary in India today?

Building on our comprehensive personal finance guide, continuing with questions 51 to 100 allows you to branch into advanced macroeconomic realities, tax structures, banking hacks, and broader psychological perspectives to complete your ultimate high-conversion content asset.

Part 6: Advanced Wealth Management & Psychological Traps

Q51. What is “revenge spending” and how does it fuel the millennial debt loop?

Revenge spending occurs when individuals overspend on luxury items, high-end dining, or premium travel to make up for perceived lost time, intense corporate work pressure, or burnout. It acts as an expensive emotional coping mechanism that quietly drains monthly savings.

Q52. Why does a high CIBIL score sometimes make it easier to fall into a debt trap?

A high CIBIL score proves you are a reliable borrower, prompting banks to continuously flood your inbox with pre-approved loans, immediate credit card upgrades, and frictionless personal credit lines. If you lack strict discipline, this easy access to debt makes over-leveraging effortless.

Q53. What is the danger of relying on “No-Cost EMIs” for lifestyle purchases?

While advertised as 0% interest, no-cost EMIs often bundle hidden processing fees, lose out on immediate cash discount opportunities, and lock up a significant portion of your future monthly cash flow, leaving you vulnerable if an emergency hits.

Q54. How does the “Diderot Effect” secretly drain a tech professional’s savings?

The Diderot Effect states that obtaining a new possession often triggers a spiral of consumption that leads to additional, unplanned purchases. For example, buying a premium electric bike often subconsciously forces you into buying expensive riding gear, high-end accessories, and specialized insurance.

Q55. What is the fundamental difference between an “Asset” and a “Liability” for urban households?

An asset puts money into your pocket over time (like equity mutual funds, commercial real estate, or dividend stocks). A liability takes money out of your pocket consistently (like a depreciating luxury car, tech gadgets on EMI, or high-rent apartments).

Q56. Why is an education loan considered “good debt” compared to a personal loan?

Education loans generally feature lower, structured interest rates, offer dedicated tax benefits under Section 80E, and directly increase your primary earning potential, whereas personal loans carry high interest rates and fund purely depreciating items or immediate crises.

Q57. How can the “50/30/20 Rule” be modified for someone trying to pay off massive loans?

When handling intense liabilities, the rule flips into a Debt-First Allocation: 50% goes to survival needs (rent, basic food), 40% is aggressively funneled into loan repayments, and the remaining 10% is strictly capped for baseline variable expenses and minimal survival cash.

Q58. What is the psychological concept of “Mental Accounting” in personal finance?

Mental accounting is the tendency for people to treat money differently based on its source or intended use. For instance, someone might recklessly spend a ₹50,000 corporate festival bonus on a luxury watch while simultaneously struggling to pay off a high-interest credit card balance.

Q59. Why do high earners often neglect building a basic liquid emergency fund?

High corporate earners frequently mistake their high monthly cash flow or large credit card limits for actual liquid financial security, leaving them highly exposed if they face sudden corporate restructuring, layoffs, or health emergencies.

Q60. How does a “paycheck-to-paycheck” cycle impact workplace productivity and mental health?

Living without a savings cushion causes severe chronic stress, sleep disruption, and low-level panic. This anxiety drains your cognitive focus, making you highly risk-averse at work and terrified of taking career risks or switching companies.

Part 7: Navigating Indian Banking Realities & Tax Optimization

Q61. Can a personal loan balance be transferred to another bank for a lower interest rate?

Yes. Through a Balance Transfer (BT) process, you can move an active high-interest personal loan to a competing bank offering a lower interest rate, helping to reduce your monthly EMI or shorten your total loan tenure.

Q62. Are there hidden charges involved when prepaying or foreclosing a personal loan in India?

Yes. Most Indian banks levy foreclosure or part-prepayment penalties ranging between 2% and 5% of the principal balance outstanding, though some banks waive this fee after a specific number of initial EMIs are cleared.

Q63. How does Section 80E benefit professionals who are paying off education loans?

Section 80E of the Income Tax Act allows you to claim a complete deduction on the entire interest component of an education loan for up to 8 consecutive years, significantly lowering your overall taxable income.

Q64. What is a “Top-Up Loan,” and should someone in debt use it?

A top-up loan is an additional loan offered by your bank on top of an existing active loan (like a home loan). While its interest rate is lower than a standard personal loan, using it to fund luxury items or lifestyle creep only lengthens your debt loop.

Q65. Why is a credit card cash withdrawal considered the worst financial move?

Withdrawing cash using a credit card triggers immediate, compounding transaction fees (often up to 3% to 5%) and carries a massive interest rate (up to 42% per annum) that begins accumulating the exact day the cash is withdrawn.

Q66. What is the “Rule of 72” and how does it help a middle-class saver?

The Rule of 72 is a quick formula to determine how long it will take for your money to double. Divide 72 by your expected annual rate of return; for example, an equity fund yielding 12% will double your investment investment in roughly 6 years.

Q67. How do quick-commerce and instant grocery apps quietly alter a household’s monthly budget?

By removing shopping friction, these apps encourage frequent, impulsive micro-orders with hidden delivery fees, handling charges, and surge pricing, driving up baseline grocery costs by 20% to 30% compared to planned weekly market trips.

Q68. What are the tax implications of taking a financial gift from parents to pay off a loan?

Under current Indian tax laws, any monetary gifts received from direct “relative” definitions (including parents, spouses, and siblings) are completely exempt from income tax, making it a safe avenue to clear high-interest informal loans.

Q69. Can a bank automatically seize funds from your savings account to clear a credit card debt?

Yes, under the “Right of Set-Off,” a bank holds the legal right to cross-verify and transfer funds from your active savings or current account to clear overdue liabilities or defaults linked to a credit card or loan held within the same banking institution.

Q70. Why is a term insurance policy critical for a family’s primary earner?

If the primary earner passes away unexpectedly, a term insurance policy provides a massive, tax-free lump-sum payout to the dependents, ensuring that outstanding personal loans, home mortgages, or family debts do not burden the surviving family members.

Part 8: Strategic Debt Management & Generational Wealth

Q71. What is the difference between reducing interest rate and flat interest rate calculation?

A flat rate calculates interest on the entire original loan amount throughout the tenure, making it highly expensive. A reducing rate calculates interest solely on the remaining principal balance outstanding month by month, which is far more consumer-friendly.

Q72. How can automated mutual fund SIPs protect millennials from their own spending habits?

Setting up automated Systematic Investment Plans (SIPs) to execute on the exact day your salary hits ensures you “Pay Yourself First.” It moves your investment allocation out of your primary spending account before impulsive discretionary spending can occur.

Q73. Is it wise to break a long-term Public Provident Fund (PPF) to clear an active personal loan?

If the personal loan interest rate (typically 13%+) is significantly outlasting the tax-free growth rate of your PPF (currently around 7.1%), clearing the high-interest drag early is often mathematically sound, provided you don’t compromise your foundational retirement safety net.

Q74. How does taking an “EMIs on Credit Card” offer differ from a bank personal loan?

Credit card EMIs are fast and do not require lengthy documentation, but they often carry higher underlying interest rates (14% to 18%), instantly block your available credit limit, and levy a 18% GST charge on the interest component.

Q75. What is the “Velocity of Debt Recovery” for young couples?

It is the speed at which a household reduces its total outstanding debt liabilities. Increasing this velocity involves finding secondary income streams, selling off non-performing assets, and funneling all surprise cash bonuses directly toward principal prepayments.

Q76. Why should young couples establish separate emergency funds from their parents?

To maintain clean financial boundaries and prevent sudden domestic emergencies (like a parent’s local business loss or an ad-hoc local liability) from completely depleting the couple’s core survival capital or stopping their wealth building.

Q77. What role does mutual fund diversification play during high-inflation economic cycles?

Diversification distributes your investment capital across large-cap, mid-cap, and sector-focused funds, protecting your core wealth from sudden domestic market sector corrections and helping your portfolio outpace retail inflation.

Q78. Can a student loan be claimed as a tax benefit if paid by a spouse?

Yes. Under Section 80E, if you are legally responsible for paying the interest on an education loan taken for your spouse, you can claim the full tax deduction against your individual corporate income.

Q79. Why do financial planners warn against investing in real estate using short-term personal credit lines?

Real estate is a highly illiquid asset that takes months or years to sell. Funding it via short-term, high-interest personal credit lines creates a severe cash-flow mismatch that can lead to rapid financial distress if property values stall.

Q80. How can compounding interest work against an individual in a middle-class household?

When you carry revolving credit card balances or high-interest personal debts, compounding interest works in reverse. The unpaid interest component stacks directly onto your principal, rapidly ballooning your total liability out of control.

Part 9: Real-World Scenarios, Case Studies, and Future Planning

Q81. What should a professional do if they cannot pay their upcoming monthly EMI?

Approach your lending bank immediately before the deadline passes. Be transparent about your cash-flow crisis, present your employment records, and request a temporary EMI holiday (moratorium) or a structured loan tenure extension to lower the payment amount.

Q82. How does a single credit card default impact your long-term ability to buy a house in India?

A single credit card default drastically lowers your CIBIL score, flags your profile as high-risk across central banking networks, and can cause banks to reject your future long-term home loan applications for several years.

Q83. What is a “Zero-Based Budget” and how can it rescue a struggling household?

A zero-based budgeting system requires you to assign every single rupee of your monthly income a distinct, explicit function (Income minus Expenses equals Zero). This ensures that no unaccounted cash slips away unnoticed on casual micro-transactions.

Q84. Why are liquid mutual funds preferred over traditional bank savings accounts for emergency money?

Liquid mutual funds provide comparable safety while reliably delivering slightly higher returns than standard bank savings accounts, all while maintaining fast withdrawal processing times for sudden domestic emergencies.

Q85. How can young professionals approach their parents regarding transparent family debt conversations?

Frame the discussion around long-term stability rather than blame. Sit down with a clear ledger, ask for all active informal liabilities to be listed explicitly, and work together to build an institutional refinancing plan to stop high-interest cycles.

Q86. What is the primary risk of co-signing a loan for a friend or relative?

As a co-signer, you assume full legal and financial liability for the loan. If the primary borrower defaults or misses a payment, the bank will legally demand full repayment from you, and any missed steps will directly damage your personal CIBIL score.

Q87. Why are traditional gold investments making a strategic comeback for modern urban portfolios?

Gold functions as a reliable hedge against sudden inflation and currency depreciation. Modern options like Sovereign Gold Bonds (SGBs) provide capital appreciation pegged to market gold rates along with an added annual interest payout, completely removing storage risks.

Q88. How can a family minimize their monthly rent outlays in premium Tier-1 tech hubs?

By exploring modern co-living communities, moving to well-connected suburban neighborhoods situated slightly away from core tech corridors, or utilizing public metro links to balance lower monthly rents with reasonable daily commutes.

Q89. What is the long-term impact of choosing the “New Tax Regime” over the “Old Tax Regime” for high earners?

The New Tax Regime offers lower direct slab rates but removes standard deductions like Section 80C, 80D, and HRA. High corporate earners must run a personalized calculation based on their active loan interest claims to choose the most efficient option.

Q90. How can an urban household reliably gamify their monthly savings targets?

By launching fun milestone challenges within the home—such as a “No-UPI Spending Weekend” or matching every rupee spent on outside dining with an identical deposit straight into a dedicated holiday or investment bucket.

Part 10: High-Traffic Meta Context & Regional Insights (Special Election Edition)

As an editorially agile platform, embedding high-traffic political, current affairs, and local governance FAQs within major lifestyle trends is a powerful way to capture trending search algorithms. These final questions address the explosive developments dominating news cycles right now.

Q91. How do sweeping regional election outcomes influence middle-class consumer confidence?

Major political shifts—such as the historic, ground-shifting assembly election results where the BJP secured its first-ever government in West Bengal by crossing the halfway mark to win 207 seats—profoundly shift market sentiment, local real estate trends, and regional business investments.

Q92. What was the defining political upset in the recent southern assembly elections?

Actor-turned-politician Vijay made a stunning debut in Tamil Nadu, with his party, the Tamilaga Vettri Kazhagam (TVK), winning 105 seats. This dramatic victory completely upended traditional state politics and challenged long-established regional party models.

Q93. What is causing the intense post-election political deadlock in Tamil Nadu right now?

The political landscape remains tense as negotiations over government formation continue. Even with TVK winning 105 seats, the DMK (59 seats) and AIADMK (46 seats) maintain significant influence. Rumors regarding the potential resignation of 108 TVK MLAs if rival coalitions stake a claim have added to the high-stakes political suspense.

Q94. Will TVK form the government in Tamil Nadu following the 2026 assembly results?

While TVK chief Vijay staked a formal claim with the Governor based on his strong seat count, uncertainty remains. The situation grew complex when the IUML publicly rejected reports of its support for TVK, making a definitive majority declaration dependent on crucial decisions from other parties like the VCK.

Q95. How does a prolonged political deadlock affect local retail inflation and real estate prices?

Extended governance delays or sudden shifts in leadership can cause short-term slowdowns in local infrastructure approvals, affecting regional employment trends, corporate expansion plans, and property valuations in key tech hubs like Chennai.

Q96. What strategy can content creators use to tie political news to personal finance articles?

Link macro policy updates directly to your readers’ wallets. For example, analyze how new state administrations handle local welfare schemes, middle-class tax structures, utility subsidies, or public transportation pricing.

Q97. Why do breaking sports events see massive search traffic spikes alongside economic news?

Audiences naturally seek a mix of serious economic updates and engaging entertainment. Major milestones—such as Shreyas Iyer’s bold first statements after being named India’s new T20I captain—frequently match or exceed political trends in search volume.

Q98. How can InstantNews use high-traffic tags to maximize visibility on Google Discover?

By strategically grouping cross-industry trending terms. Combining financial tags like #PersonalFinance and #LifestyleCreep with high-volume current affairs tags like #WestBengalElections, #TVKVijay, and #ShreyasIyer helps your articles capture multiple active user interests.

Q99. What format works best for presenting complex multi-topic news trends?

Use high-contrast bulleted summaries, scannable comparison tables, and interactive polls. This approach holds a reader’s attention much longer than dense paragraphs, lowering bounce rates and signaling quality to search algorithms.

Q100. How can readers contribute their own perspectives to this growing national discussion?

Drop your thoughts in our comment section below! Let us know how you are navigating middle-class lifestyle inflation, share your perspective on the changing political landscape in Tamil Nadu and West Bengal, and tell us what topics you want our team to break down next!

This video on Millennial Debt Traps and Financial Planning Tips provides helpful context on the broader political and economic factors that influence urban living costs, which are directly related to the personal finance topics and middle-class budget traps explored in this FAQ.