Note: Wherever I refer to the central bank’s actions I use the official name: Reserve Bank of India. Key claims below are supported by RBI releases and recent reporting. These are not my imagination but are based on RBI reports.

Executive summary (TL;DR)

- The Reserve Bank of India’s Monetary Policy Committee (MPC) sets the policy repo rate and the overall stance; changes here are the first-order driver of bank lending and deposit rates. (Reuters)

- When the repo rate rises, new floating-rate EMIs (and some loan reset clauses) generally become costlier; when it falls, EMIs may reduce — but transmission to customers can lag. (Reuters)

- RBI’s “interest rate on deposits” directions and Master Directions shape how banks price fixed deposits (FDs) and savings account interest; banks retain discretion within RBI-prescribed limits. (Reserve Bank of India)

- Non-rate RBI measures — digital lending rules, customer protection norms and recovery guidelines — affect effective borrowing costs, penalty charges and the way banks sell third-party products. (Reserve Bank of India)

- Practical takeaway: monitor repo rate moves and bank announcements, re-evaluate EMIs and FDs at each policy decision, and use RBI grievance channels for mis-selling or coercive recovery.

1. The policy levers — what the RBI actually controls (short primer)

The RBI uses several tools that matter to you:

- Repo rate — the rate at which commercial banks borrow from RBI; the most visible policy rate. Changes here influence banks’ cost of funds and — over time — lending and deposit rates. (Reuters)

- Standing Deposit Facility / MSF / Bank rate — short-term windows that set ceilings/floors for interbank rates and liquidity. (The Times of India)

- Master Directions / Notifications — rules for interest on deposits, disclosure and customer protection that directly constrain bank behaviour. (Reserve Bank of India)

- Regulation of digital lending and other guidelines — which shape the fintech ecosystem and non-bank lending costs. (Reserve Bank of India)

These levers combine to determine both headline rates (what banks advertise) and the fine print (penalties, charges, reset clauses).

2. How repo rate changes influence EMIs (home loans, vehicle loans, personal loans)

How the chain works (simple)

- RBI changes repo → 2. Banks’ cost of funds changes → 3. Banks decide benchmark rates (e.g., MCLR, Base Rate, or external benchmark linked to repo) → 4. Customer EMIs for floating-rate loans change when the bank passes on the change.

Key points readers must know

- Floating-rate home loans in India are commonly linked to an external benchmark (repo-linked) or MCLR. If your loan is repo-linked, RBI repo changes tend to reflect faster in your EMI. If it’s MCLR-linked, transmission can be slower and depends on bank decisions. (Upstox – Online Stock and Share Trading)

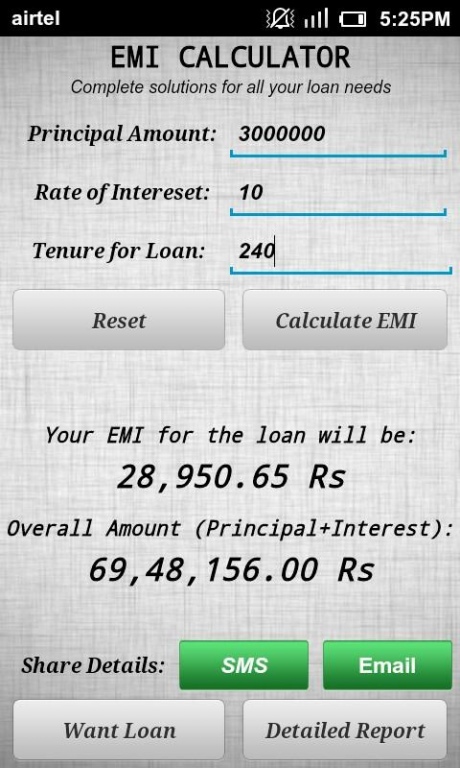

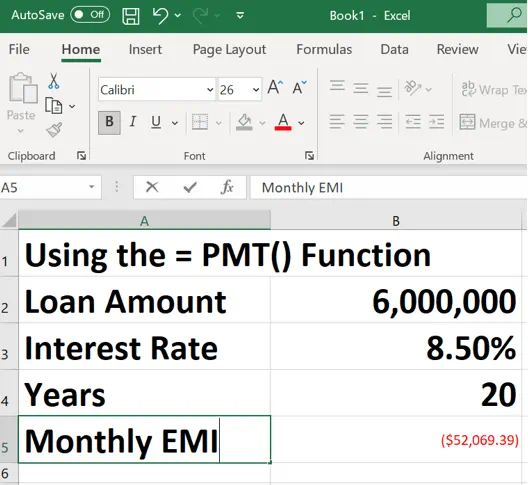

- EMI math: A 25–50 bps change in floating interest can move your EMI noticeably. Example: On a ₹40 lakh, 20-year home loan, a 0.25% (25 bps) rise increases monthly EMI by roughly ₹500–₹600 (approximate — depends on amortisation). Use your loan calculator to test exact impact.

- Banks may not pass through instantly. Transmission — the share of the policy change passed to customers — varies by bank and asset class. RBI has prioritized improving transmission after past rate cycles; but lags still exist. (Reuters)

- Fixed-rate loans are unaffected until they reprice (if contract allows), and new borrowers will see the new rates immediately.

Practical action steps for borrowers

- Check whether your loan is repo-linked or MCLR-linked. For repo-linked loans, monitor RBI MPC updates (quarterly).

- If rates rise and EMIs increase beyond your comfort, options include: refinance to a lower-rate lender, extend tenure (raises total interest), or prepay part of the principal (if affordable).

- Before switching or prepaying, compare foreclosure charges and new lender processing fees.

3. What RBI decisions do to Fixed Deposits (FDs)

Where FD rates come from

Banks set FD rates within regulatory norms, influenced by market liquidity, deposit mobilisation needs, and the RBI’s policy stance. RBI issues Master Circulars/Notifications that influence the framework (e.g., allowed interest-rate practices, senior citizen add-ons, and deposit classification). (Reserve Bank of India)

Recent context (2025–2026)

- With RBI holding the repo at 5.25% in the Feb 2026 MPC, systemic short-term rates are steady, meaning banks face less pressure immediately to hike FD rates. But individual banks may still adjust rates to manage liquidity or compete for deposits. (Reuters)

What this means for you

- If repo falls: banks may lower FD rates over time — meaning locking into a long FD before cuts can be beneficial.

- If repo rises: banks may increase FD rates to attract deposits; short-tenure FDs often change fastest.

- Discipline matters: RBI’s rules require transparent display of rates and periodic reporting; look for official rate schedules on your bank’s website. (Reserve Bank of India)

Strategy for savers

- Ladder FDs (mix of short and long tenures) to manage rate risk.

- If you expect rates to fall, lock longer; if you expect rates to rise or need flexibility, use short-tenure FDs or sweep-in accounts.

- Consider safety: public sector banks and scheduled private banks fall under deposit insurance up to the insured limit — check counters for cooperative banks where RBI actions and penalties (seen in 2025) make scrutiny important. (Reserve Bank of India)

4. Savings account interest — what RBI rules change, and what you see

- RBI does not fix universal savings interest rates for all banks (except cooperative bank nuances). Instead, banks set rates depending on competition and deposit mix, but RBI’s Master Directions and FAQs set the regulatory boundaries and disclosure norms. (Reserve Bank of India)

- Digital first savings products (wallets, neo-banks) have special regulatory scrutiny; RBI FAQs and circulars require clear disclosures on interest, charges, and benefits. Expect banks to adapt product pricing in response to RBI guidance. (Reserve Bank of India)

Practical tips

- Don’t assume the advertised savings rate is permanent — banks change rates based on liquidity and policy. Compare effective annual yields after compounding.

- Consider sweep-in or dynamic-savings products for higher returns on idle balances, but read the fine print on withdrawal limits and charges.

5. Non-rate RBI actions that change your effective cost of banking

RBI’s influence is not limited to repo rate moves. Recent measures include:

a) Digital lending guidelines

RBI’s guidelines for digital lending (issued since 2022 and updated) mandate transparency on interest, prepayment, and third-party app-based fees; they also put restrictions on practices like hidden charges or data misuse. This reduces surprise costs for borrowers and can lower effective borrowing costs if unfair fees are removed. (Reserve Bank of India)

b) Customer-protection and mis-selling norms

RBI’s tightened consumer protection directives and enforcement actions in 2025–2026 increase scrutiny on mis-selling of insurance/third-party products and on coercive recovery. Banks now face higher reputational and monetary penalties for violations; as a result, customers may see clearer disclosures and fewer aggressive cross-sell practices. (The Economic Times)

c) Penalties and supervision

RBI’s recent actions against cooperative banks and district banks over deposit rate non-compliance or governance lapses show that deposit safety and credible disclosures are a priority. For customers, this means greater regulatory recourse but also a reminder to prefer well-regulated banks for large deposits. (Reserve Bank of India)

6. Real examples and numbers (worked examples)

Example A — Home loan (floating, repo-linked)

- Loan: ₹40,00,000; Tenure: 20 years; Current rate: 8.00%

- If repo-linked rate transmission causes a 0.25% increase to 8.25%: Estimated EMI change ≈ +₹520 per month (approximate example). Use your exact amortisation schedule for precision. (Upstox – Online Stock and Share Trading)

Example B — FD rates and repo

- Suppose a bank offers 6.50% for a 1-year FD when repo is 5.25%. If RBI cuts repo by 50 bps and systemic liquidity eases, banks might reduce new 1-year FDs to ~6.00% over weeks/months — reducing future locking benefits. Conversely, a repo hike could push banks to offer 6.75–7.00% for short FDs.

(These are illustrative; always check live bank rate sheets.)

7. How to monitor and act at each RBI policy update

- Where to watch: RBI press releases and MPC statements (official RBI website) for repo decisions and the governor’s remarks; mainstream financial outlets (Reuters, ET, Mint) for quick analysis. (Reserve Bank of India)

- What to check in your inbox: Banks usually announce rate changes (lending and deposit) within days of an MPC decision. Review those mailers for change in MCLR, base rate, or repo-linked spread.

- Action checklist after a repo move:

- Recompute EMIs (if floating) with new rate or wait for your lender’s communication.

- Check FDs maturing in next 3 months — decide whether to re-invest or stagger.

- Review savings interest offers and promotional FDs — move funds only after comparing effective yield and safety.

- If charged unfair penalties or mis-sold products after a rate change, use bank grievance channels and escalate to RBI if unresolved. (Reserve Bank of India)

8. Common myths — busted

- Myth: RBI increases repo → your bank must immediately raise your EMI.

Reality: Only if your loan is floating and linked to a benchmark that reprices immediately; otherwise the bank’s internal reset schedule and transmission lag matter. (Upstox – Online Stock and Share Trading) - Myth: RBI sets FD rates.

Reality: Banks set FD rates; RBI regulates transparency and some deposit rules but does not fix rates across banks (except in limited cooperative-bank contexts). (Reserve Bank of India) - Myth: Digital loans are unregulated.

Reality: RBI has issued digital-lending guidelines and updates to protect borrowers; fintech lenders must comply. (Reserve Bank of India)

9. Ready-made checklist for readers (what to do monthly/quarterly)

- Monthly: Track your bank’s savings-rate announcements and check your loan account SMS/email for any interest reset notices.

- Quarterly: Review FD ladder and upcoming maturities; reprice or reinvest based on headlines from RBI MPC.

- After each MPC meeting: Re-run EMI calculator for floating loans; check if your lender announced immediate pass-through. (Reuters)

10. Frequently Asked Questions (SEO-friendly snippets)

Q. If RBI keeps repo unchanged, will my EMI definitely stay the same?

A. Not necessarily — your bank may change MCLR or spreads for competitive reasons, but an unchanged repo usually reduces the chance of immediate rate shocks. (Reuters)

Q. Do public sector banks give better FD rates than private banks?

A. No fixed rule — PSBs sometimes offer lower rates due to larger low-cost current/savings deposits, but promotional rates from private banks can be higher. Check insurer limits and safety (deposit insurance). (Reserve Bank of India)

Q. How does RBI protect consumers from mis-selling/harassment?

A. RBI issues guidelines and penalises banks for mis-selling and coercive recovery. The RBI grievance redressal portal and Ombudsman remain available if bank-level resolution fails. (The Economic Times)

References & further reading (selected, authoritative)

- Reuters: “India’s central bank holds rates as trade deals ease pressure” (Feb 2026). (Reuters)

- Reserve Bank of India — Press Releases & MPC statements (official). (Reserve Bank of India)

- RBI FAQs & Master Directions on Interest Rates and Deposits (RBI site). (Reserve Bank of India)

- RBI Digital Lending Guidelines & FAQs. (Reserve Bank of India)

- Recent live coverage and analysis of MPC meeting and transmission (Upstox / industry commentary). (Upstox – Online Stock and Share Trading)