Aaiye samjhte hai CIBIL Score kaise kaam karta hai, iska apki life pe kya impact hai aur jaldi se apna CIBIL score kaise improve kare

Aaj ke time me agar aapko credit card, home loan, car loan ya koi bhi aur typpe ka loan chahiye, to sabse pehle bank ek hi cheez check karta hai:

👉 Your CIBIL Score

Agar CIBIL score low hai, to:

- Loan reject hoga ❌

- Interest rate bohat high 💸

- credit limit kaafi kam hogu 😑

Lekin problem ye hai ki 90% logon ko ye pata hi nahi hota ki CIBIL score actually works kaise karta hai.

Aaj is article me hum simple Hinglish me samjhenge:

- CIBIL score kya hota hai

- CIBIL score kaise calculate hota hai

- CIBIL score kaise fast improve karein

✅ What is CIBIL Score? (Simple Explanation)

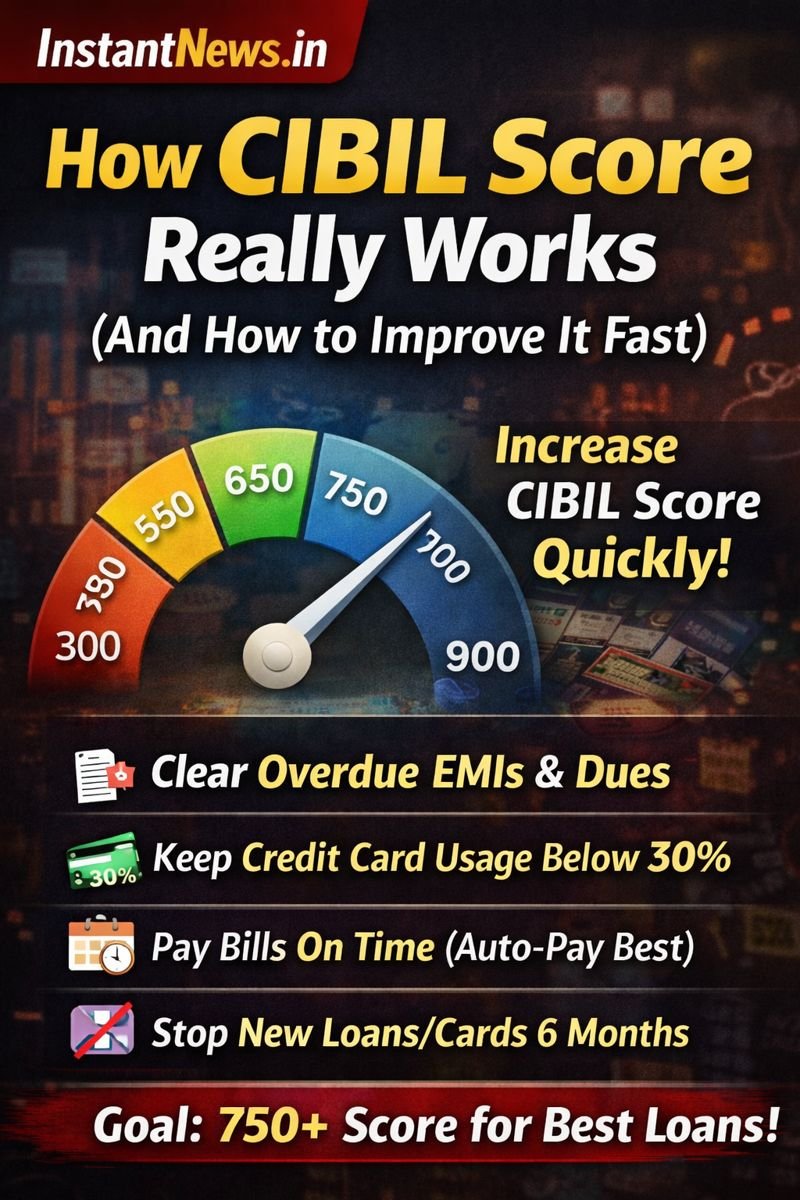

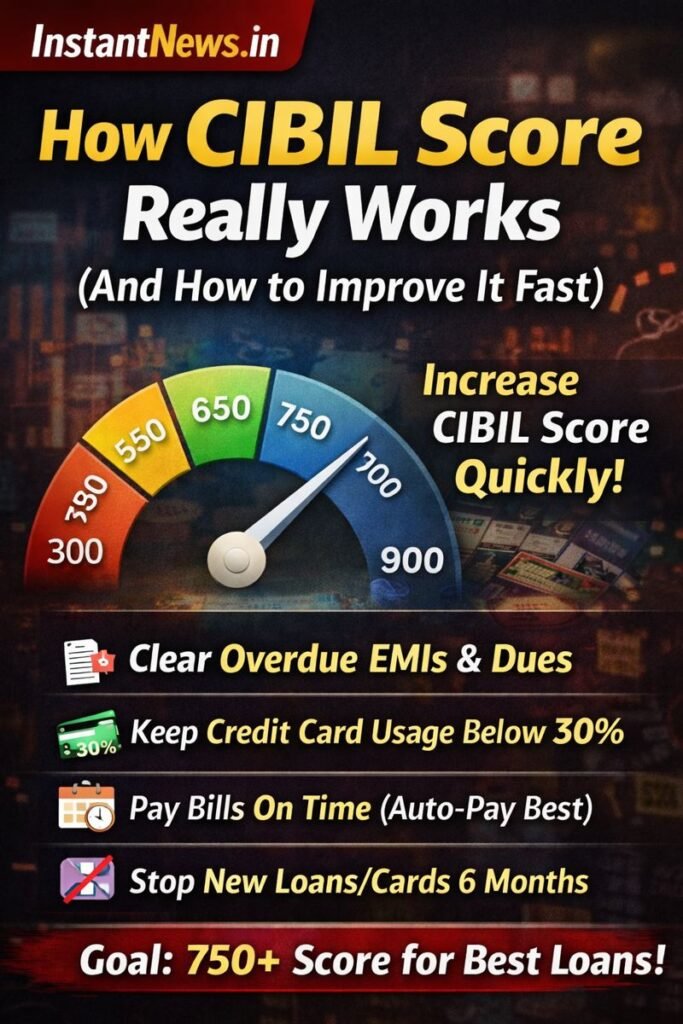

CIBIL Score ek 3-digit number hota hai (300 se 900 ke beech) jo aapki credit history dikhata hai.

- 750+ = Excellent score ✅

- 700–749 = Good 🙂

- 650–699 = Average 😐

- Below 650 = Risky ❌

Higher score = Bank ko lagta hai aap safe borrower ho.

⚙️ How CIBIL Score Really Works? (Behind the Scenes)

CIBIL score mainly 4 cheezon pe depend karta hai:

1. Payment History (Sabse Important – ~35%)

Aap EMI aur credit card bill time pe bharte ho ya nahi

- 1 bhi late payment = score down ⬇️

- Zyada missed payments = heavy damage 🚨

2. Credit Utilization Ratio (~30%)

Aap apni credit limit ka kitna % use kar rahe ho?

Example:

- Credit limit = ₹1,00,000

- Aap use kar rahe ho = ₹90,000 ❌ (Very bad)

- Best = Below 30% usage ✅

3. Credit History Length (~15%)

Aap kitne time se loan / credit card use kar rahe ho?

Purana, clean record = better score

Isliye old credit card kabhi bina reason band mat karo

4. Credit Mix & New Loans (~20%)

- Sirf credit cards ❌

- Sirf personal loans ❌

- Mix of home loan + card + auto loan ✅ (Healthy profile)

Aur:

Bahut saare loans / cards ek saath apply karoge = score down ⬇️

🚨 Biggest Reasons Why CIBIL Score Falls

- EMI late payment

- Credit card bill minimum amount only pay karna

- Limit se zyada credit use karna

- Bahut zyada loan applications

- Settlement / write-off / default

🚀 How to Improve CIBIL Score Fast (Proven Methods)

✅ 1. Sabse Pehle Overdue Clear Karo

Pending EMIs + credit card dues = priority #1

✅ 2. Credit Card Usage 30% Ke Andar Lao

Agar limit 1 lakh hai → usage 30,000 ke andar rakho.

✅ 3. Har Payment Time Pe Karo (Auto-Debit On Karo)

✅ 4. New Loans & Cards Apply Karna Band Karo (3–6 months)

✅ 5. Minimum Due Nahi, Full Bill Pay Karo

✅ 6. Apni CIBIL Report Check Karo

Kabhi kabhi:

- Galat loan entries

- Closed loan still showing open

- Wrong late payment marks

Inko dispute karne se score improve ho jata hai.

⏳ How Fast Can CIBIL Score Improve?

- 1–2 months: Small improvement

- 3–6 months: Good improvement

- 6–12 months: Major recovery (agar discipline follow kiya)

❓ What Is a Good CIBIL Score to Get Loan Easily?

🎯 750+ CIBIL score = Best loan offers + low interest rates

🧠 Big Truth About CIBIL Score

CIBIL score koi magic se improve nahi hota.

Ye discipline + time + consistency se hi banta hai.

✅ Bottom Line

Agar aap:

- Time pe payment

- Low credit usage

- Kam loan applications

- Clean credit history

Rakhte ho → CIBIL score automatically strong ho jaata hai wo bhi bohat tezi se. RBI ki nayi guideline ke hisab se ab CIBIL score har 15 din me update hoga aur ye step apke liye kafi useful sabit ho sakt hai

📝 Recommended Related Articles for you

Chandi 3 mahine me double kaise ho gayi aur aage kaha jayegi?